By Deodatus Balile, JamhuriMedia, Dar es Salaam

The sudden narrative suggesting that Nigerian billionaire Aliko Dangote has shifted interest from Tanzania’s Tanga to Kenya’s Mombasa deserves careful scrutiny. A closer look at infrastructure realities, regional logistics, electricity capacity, land availability, and market geography shows that Tanzania still holds the stronger long-term strategic advantage for a mega refinery intended to serve Eastern and Central Africa.

At the centre of this debate is a proposed refinery worth between $15 to $17 billion, modelled on the 650,000-barrel-per-day Dangote refinery in Nigeria. Reuters and the Financial Times recently reported that Dangote was “leaning more towards Mombasa because Mombasa has a much larger, deeper port.”

But the available facts do not fully support the emerging perception that Mombasa is economically superior to Tanga for such a continental-scale refinery project.

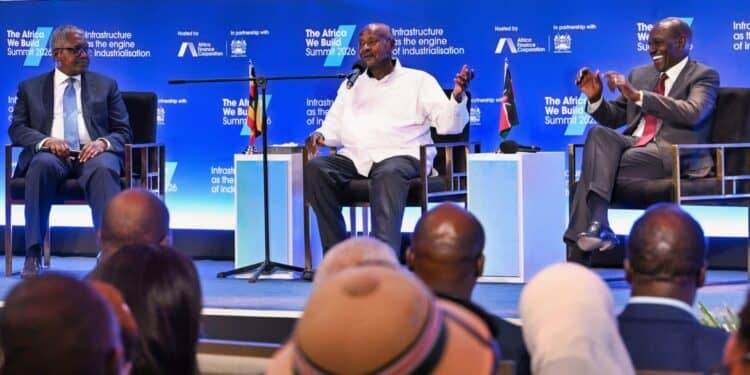

What remains publicly documented is that during the Africa We Build Summit in Nairobi on April 23, 2026, Dangote made a direct commitment before Kenyan President William Ruto and Ugandan President Yoweri Museveni regarding a refinery in Tanga, Tanzania.

“We are discussing the establishment of a joint refinery in Tanga to benefit all of us,” President Ruto declared publicly. Reuters further reported that the refinery would process crude from Uganda, South Sudan, Kenya and the Democratic Republic of Congo.

Dangote himself stated: “My commitment today here is that if we agree with the three or four governments here about the refinery, we will lead and we’ll make sure that refinery is built within the next four or five years.” He added even more firmly: “If they will support the refinery, we’ll build the identical one that we have in Nigeria.”

That commitment, made publicly before two sitting presidents, carries more political and economic weight than anonymously amplified interpretations of a later interview.

It is therefore legitimate to question whether the current media wave is partly driven by spin doctors attempting to psychologically shift investor sentiment and create the impression that the refinery has already migrated to Kenya. The economics themselves remain heavily tilted toward Tanzania.

First, is the issue of crude oil logistics. Tanzania already hosts the East African Crude Oil Pipeline (EACOP), a 1,443-kilometre pipeline running from Hoima in Uganda to Chongoleani near Tanga Port. This existing strategic corridor gives Tanga a natural advantage. The proposal discussed by Ruto, Museveni and Dangote envisioned crude from Uganda, South Sudan and the DRC feeding the Tanga refinery.

The numbers matter. Juba in South Sudan is approximately 568 kilometres from Hoima, Uganda, where crude could connect into EACOP infrastructure before reaching Tanga. By comparison, Juba is roughly 1,752 kilometres from Mombasa. Constructing a crude transport system across such a distance would dramatically inflate pipeline and logistics costs.

The same logic applies to the Democratic Republic of Congo. Kinshasa is about 4,430 kilometres from Mombasa. The transportation economics become increasingly difficult to justify when compared with the integrated EACOP-Tanga model already under construction.

Secondly, market geography favours Tanzania more than headline population figures suggest. A refinery in Tanga would naturally serve not only Tanzania but also Uganda, Rwanda, Burundi, eastern DRC, Zambia, Zimbabwe, Malawi, Mozambique and potentially South Sudan through interconnected transport systems. This creates a broader SADC-EAC synergy than a Kenya-centred narrative acknowledges.

Kenya’s domestic market argument is also weaker than portrayed. Kenya’s economy may presently consume more petroleum products than Tanzania individually, but refinery economics are determined by regional demand corridors, logistics efficiency, export routes and industrial expansion potential — not merely one national market.

Tanzania’s geographical centrality to Southern and Central African trade routes gives Tanga a strategic distribution advantage into landlocked economies. For several inland countries, transporting refined fuel from Tanga would be significantly shorter and more economical than routing supplies from Mombasa.

Thirdly, energy availability matters enormously for a refinery of this scale. A refinery comparable to Dangote’s Nigerian complex requires vast and stable electricity supply. Tanzania currently has approximately 4,031 MW of produced electricity capacity, whilst Kenya’s installed capacity is around 2,651 MW, although politically contested figures continue to circulate in public debate.

The issue recently became more visible when a proposed $1 billion Microsoft-G42 data centre in Kenya reportedly stalled amid concerns over national electricity capacity. Reuters reported that the scale of the project raised serious questions regarding Kenya’s ability to guarantee the required power.

President Ruto himself is quoted to have issued a warning that powering the facility could require “switching off half the country.” Such realities inevitably raise questions about whether Kenya presently possesses the surplus industrial power required for a mega refinery consuming enormous continuous energy loads. His refinery facility in Nigeria is designed to be powered by a dedicated 435-megawatt (MW). With this you mean 25% of Kenya’s total produce electricity capacity.

Tanzania, meanwhile, continues expanding generation through hydropower, natural gas and transmission investments, placing it in a comparatively stronger long-term industrial position. The country is targeting a production of 8,000 megawatts (MW) come 2030.

Land availability is another overlooked factor. Kenya’s coastal industrial land around Mombasa is far more constrained and expensive than Tanzania’s relatively expansive industrial zones around Tanga and Chongoleani. Large-scale refining complexes require not only refinery space itself, but also petrochemical zones, storage terminals, pipelines, worker settlements and export infrastructure extending over vast areas. Tanzania still offers greater room for industrial expansion at comparatively lower land acquisition costs.

Critics are pointing to Tanzania’s October 29, 2025 election violence as an investor risk. Yet those events increasingly appear isolated rather than structural compared to several neighbouring countries. In a strong term, Tanzania remains the most politically stable country in the region. The Tanzanian government has since intensified efforts aimed at addressing socio-economic tensions, especially youth unemployment and political reconciliation.

Moreover, Dangote is not entering an unfamiliar market. He already has substantial investments in Tanzania through cement and other sectors. His long-standing engagement suggests that he understands Tanzania’s commercial environment well enough to distinguish temporary political turbulence from long-term industrial opportunity.

Even President Samia Suluhu Hassan, said the proposal to build the refinery in Tanga was part of wider and long standing regional industrial consultations.

The crucial point is this: the refinery concept was originally framed as a regional East African industrial project centred on Tanga, supported publicly by Ruto, Museveni and Dangote himself. For that logic suddenly to reverse entirely in favour of Mombasa would require overriding major geographical, infrastructural and economic realities.

Unless Dangote is deliberately prepared to absorb strategic losses for political or diplomatic considerations, the hard economics still favour Tanga.

Deep harbours alone do not determine refinery success. Pipelines, electricity, land, regional access, inland transport distances, political stability, export corridors and long-term industrial integration matter more. And on those fundamentals, Tanzania continues to hold the stronger hand. I hope Dangote is properly informed and watching the spin doctors at work. God bless East Africa.

Drop me a call +255784404827.

Deodatus Balile is a multiple award-winning seasoned journalist with more than 32 years of experience, particularly in economic and geopolitical reporting.